Financial sustainability of higher education providers in England: An update

This report provides a summary of the Office for Students’ (OfS’s) analysis of financial data returned by registered higher education providers in England (excluding further education colleges) to the OfS at the end of October 2020 as part of an ‘interim financial data return’.

- Ref:

- OfS 2020.56

- Date:

- 11 December 2020

Read the report in full

Download the financial sustainability update report as a PDF

Key points

- The aggregate financial position of OfS registered universities, colleges and other higher education providers is sound at the date publication of this report, with strong cash balances, despite the challenges faced as a result of the coronavirus pandemic.

- The higher education sector in England has, in general, responded well to the pandemic with sensible financial management including good control of costs. In part, this reflects stronger overall student recruitment in 2020-21 than many were predicting. Although fee income from international students in 2020-21 is forecast to fall compared to 2019-20, it is still greater than in 2018-19.

- To support financial resilience, borrowing has increased by around 5 per cent, including through some of the government-backed loan schemes. Further loan facilities have been agreed as contingency but have not yet been drawn down.

- Although the aggregate financial position is sound, there is still very significant uncertainty as the pandemic continues, so the situation could change quickly. Issues that could impact on income include higher numbers of students dropping out, reduced income from accommodation and conference facilities or impact of COVID-19 restrictions.

- As we have previously reported, there continues to be significant variability between the financial performance of individual providers. Despite this, the likelihood of multiple providers exiting the sector in a disorderly way due to financial failure is low at this time. We continue to monitor the financial position of individual registered providers and will continue to intervene if we consider that necessary to protect the interests of students.

Notes

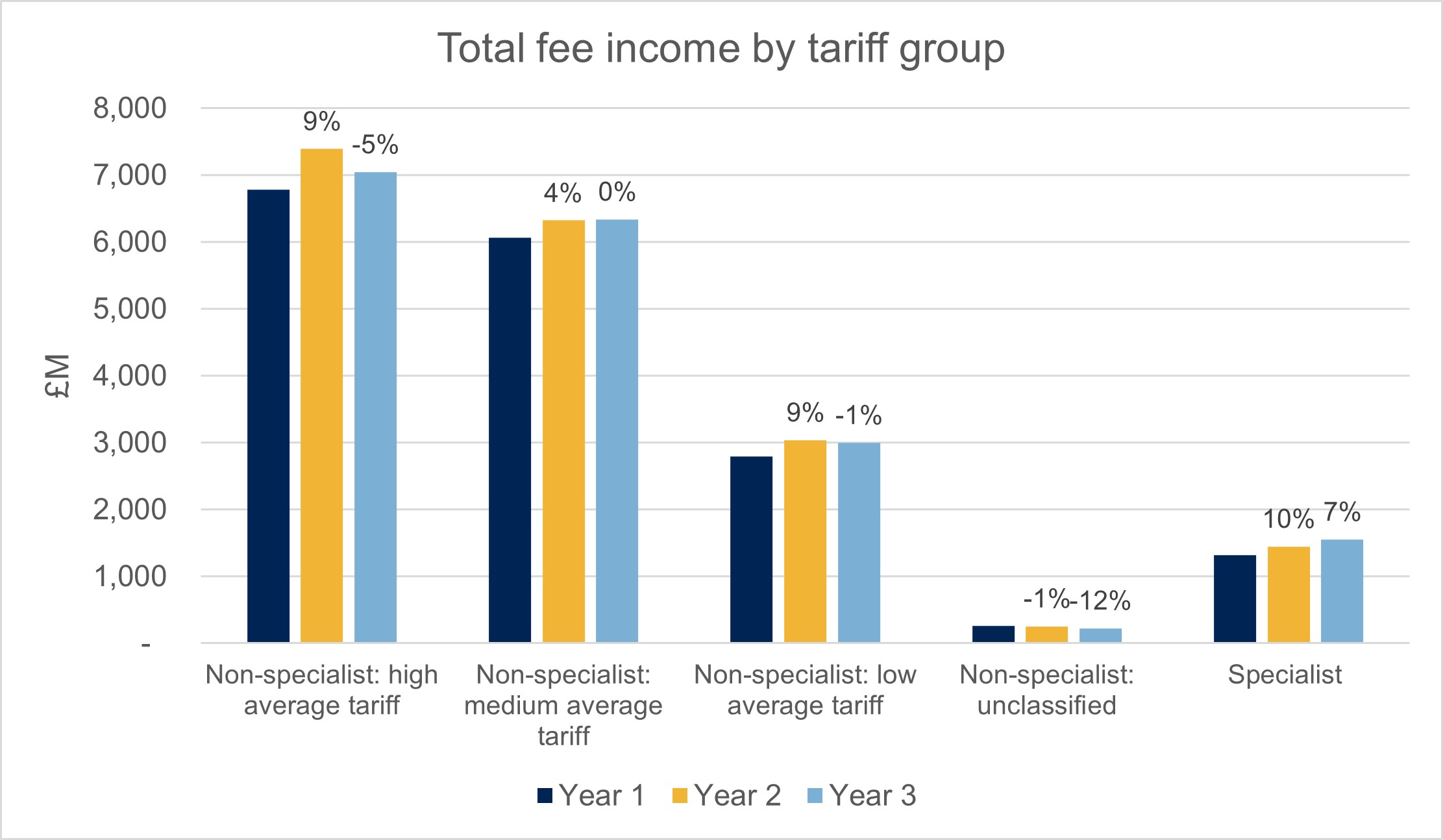

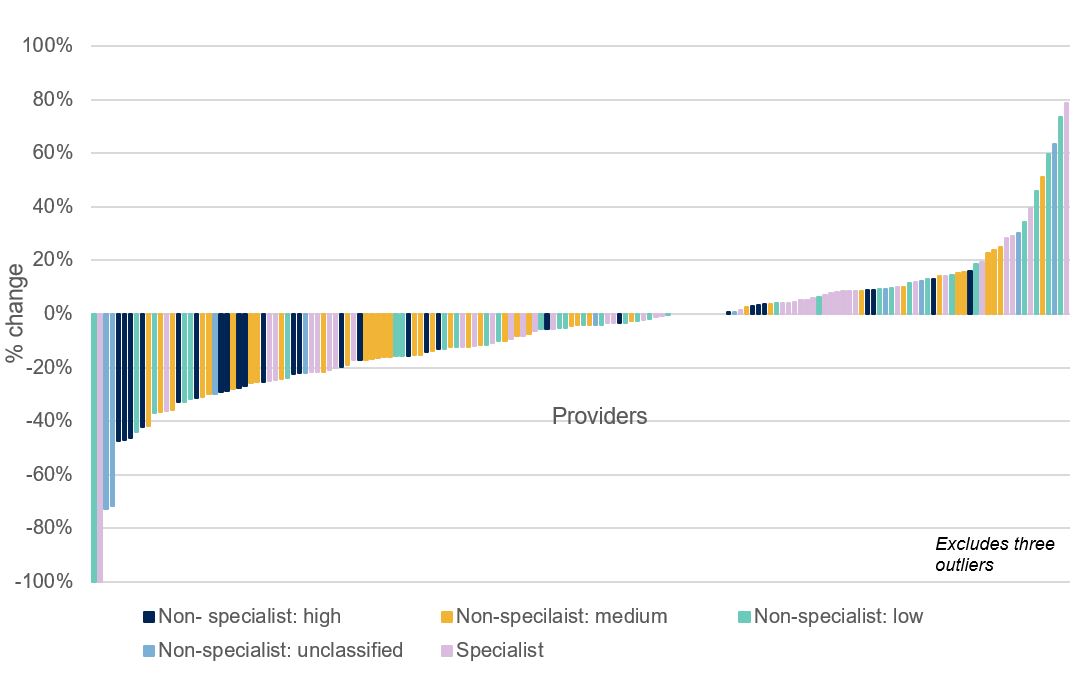

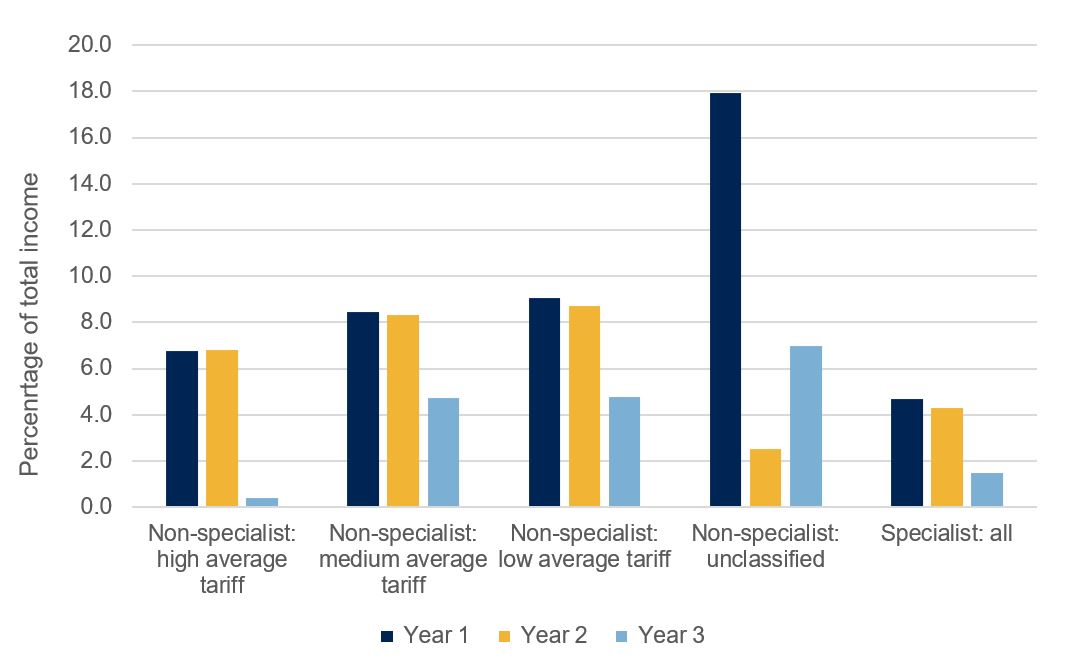

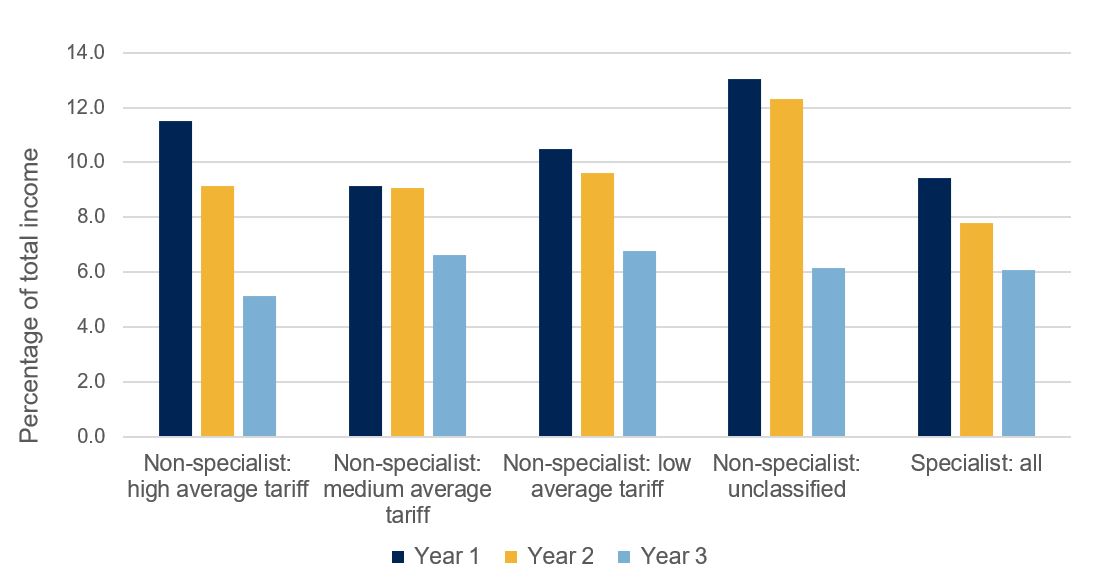

- Years: There are a variety of year end dates across providers, and so year data is sometimes referred to year 1, 2 and 3. For ease of reference, for the significant majority of providers this means 2018-19, 2019-20 and 2020-21 respectively. It should be noted that data submitted in the Interim financial data return for 2019-20 and 2020-21 is forecast and therefore unaudited.

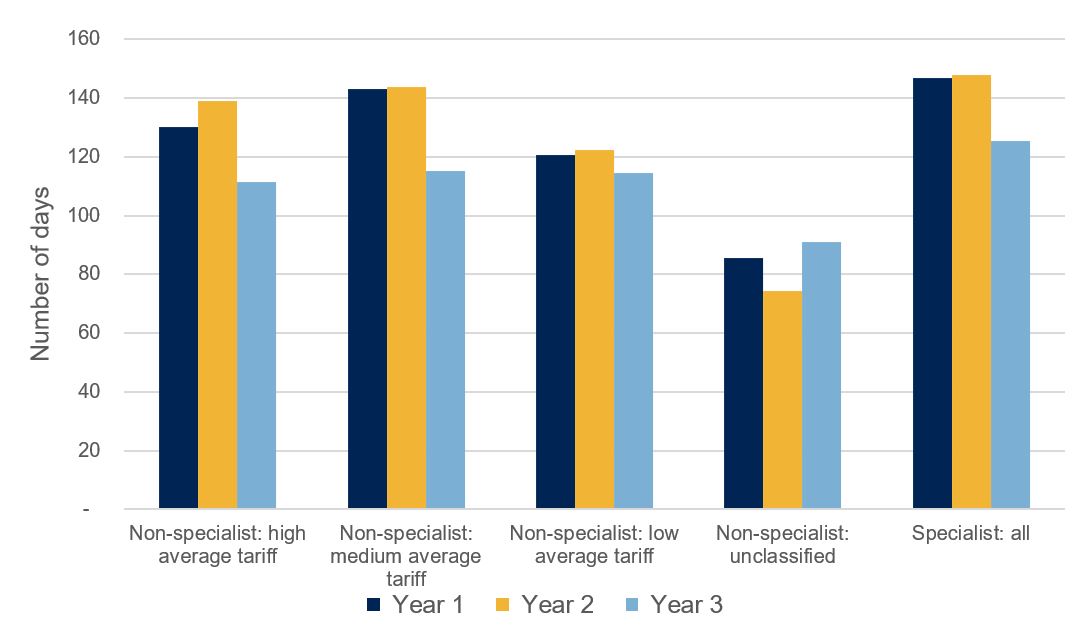

- Tariff peer groups: Three peer groups (non-specialist: high, medium and low tariff) are based on the tariff entry points of providers’ undergraduate student population. The ‘specialist: all’ group includes providers offering specialist provision (a high proportion of students concentrated in a small number of subject areas) and regardless of tariff entry points. A fifth group (non-specialist: unclassified) consists of 23 providers with no tariff classification. This group includes a diverse range of providers with different financial structures and the aggregate data in this group can be skewed by data of a few individual providers.

Explore the data in this report

Figure A1: Total fee income by tariff group

Figure A2: Overseas fee income change between 2019-20 and 2020-21 (where non-EU fee income is over 5% of total fee income)

Figure A3: Cashflow from operating activities as a percentage of total income

Figure A4: Surplus (excluding pension scheme adjustments) as a percentage of total income by tariff group

Figure A5: Liquidity days by tariff group

Describe your experience of using this website